I realize that I haven’t published in a very long time (although I’ve done a few articles in the recent past on seekingalpha.com). There hasn’t really been much to talk about. Global government stimulus has heretofore put a floor on markets – which teeter now and then but have returned to their lofty levels every time. I’ve had the urge to sell for months, but managed to talk myself out of it (just the ‘jitters’ I told myself): So why the change of heart?

I was in Europe in October of 1987 when markets plunged. On my return everything was on sale and fortunately (for the performance of the funds I was managing) I went on a buying binge. Ever since, I get anxious when September and October come around. This anxiety is peaking now, especially as I note a number of trends I find unsettling.

Interest rates at the long end of the curve have been rising. The cost of borrowing is rising.

Corporate profits have been stellar coming off the bottom of the COVID recession, but the growth rate is about to slow down. Supply remains constrained and P x Q (revenues) will in the short term have trouble increasing despite price increases. Speaking of price increases, inflation is becoming worrisome for all of us. Today’s report from the Bureau of Labor Statistics indicated the Consumer Price Index has risen 5.4% over the past 12 months. There’s nothing inherently wrong with prices rising, as long as we can afford to pay higher prices. This report from the Bureau also came out today:

Real average hourly earnings for all employees decreased 0.1 percent from June to July, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. This result stems from an increase of 0.4 percent in average hourly earnings combined with an increase of 0.5 percent in the Consumer Price Index for All Urban Consumers (CPI-U).

You feel it, I feel it and everyone we talk to feels it – incomes are not keeping up with inflation. Real estate and the stock markets have everyone ‘feeling’ wealthier, until they don’t.

All market pundits seem to be bearish and if history is any guide, September/October may prove they’re right this time. Why sell only half? If I’m right then I can buy it all back cheaper; if I’m wrong at least I can collect some dividends.

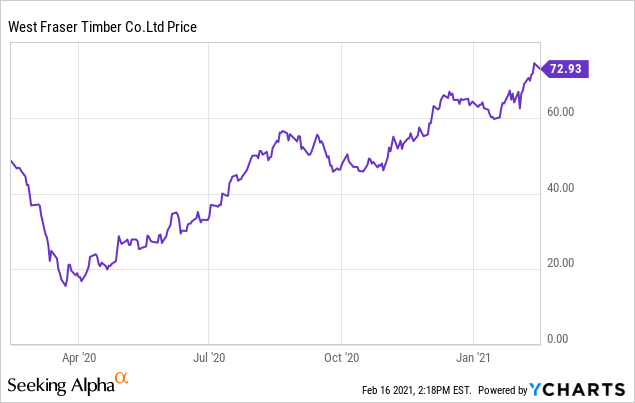

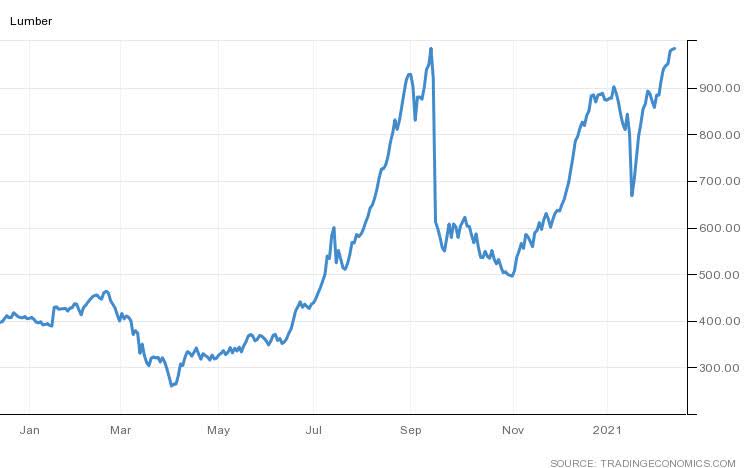

Back on August 17th, I published an article predicting that the strong housing market, increasing home improvement and renovation activity during the pandemic and rising lumber prices would benefit Canadian lumber stocks. Although no longer a secret, there remains plenty of upside in the stocks as the high lumber prices work their way into earnings for the sector.

“Privately-owned housing units authorized by building permits in December were at a seasonally adjusted annual rate of 1,709,000. This is 4.5 percent (±1.4 percent) above the revised November rate of 1,635,000 and is 17.3 percent (±1.8 percent) above the December 2019 rate of 1,457,000.”

This situation is similar in Canada. One of the stocks I featured in the article was West Fraser Timer (WFG). West Fraser is one of North America’s largest lumber manufacturers with 45 facilities in British Columbia, Alberta, and the southern U.S.

On February 1st, 2021 the company completed the acquisition of Norbord Inc., an international producer of wood-based panels (Oriented Strand Board) based in Canada. A unique buying opportunity exists in the short term as analysts work towards understanding the fundamentals of the now combined company.

Despite the pandemic, West Fraser (data prior to the acquisition) enjoyed a respectable 2020:

Sales of C$ 5.850 billion in the year

Earnings of C$776 million or 13% of sales

Adjusted EBITDA of C$1.460 billion

Cash provided by operating activities of C$1.295 billion

Invested C$241 million in capital projects

Year-end liquidity strong at C$1.619 billion and net debt to capital ratio at 2%

Norbord also reported record 2020 (in US dollars) results prior to the acquisition, with Adjusted EBITDA of $865 million for the full-year 2020 compared to $138 million in 2019. Again, the results were bolstered by high prices for OSB.

I estimate the stock is trading at only 3X EBITDA – this is one cheap stock. And the good news is that earnings corresponding to these (chart from tradingeconomics.com) high lumber prices are just beginning to drop to the bottom line.

My own expectation is that WFG trades at 5X EBITDA or at a target price of $115 to $120 in just a few months time as the earnings power of the combined companies becomes more evident. My target does not take into account obvious synergies in terms of distribution and operations afforded by the acquisition.

Stock is up 80% from when I last published about it, with plenty more to go.

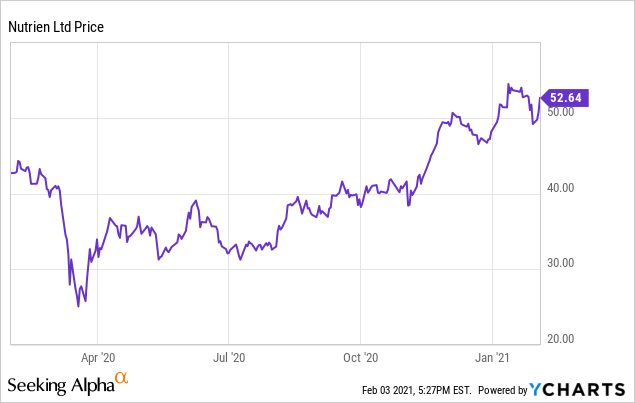

Fertilizer prices have been surging on the back of continued strong crop prices.

Global leader in potash, nitrogen and phosphate fertilizers.

When I last suggested Nutrien on March 27th, 2020 (NTR) (published on seekingalpha.com) the stock was in the neighborhood of $28 (when it was just another casualty of the coronavirus selloff). More recently the stock is slightly north of $50, but with a number of tailwinds likely to push the stock to a more compelling valuation.

Although we are all familiar with the rebound in energy prices (which makes that sector especially attractive once again) few are aware that agricultural prices have also been rising. With prices for key cash crops like corn, wheat and soybeans rising to five year highs, demand and pricing for fertilizer will be very strong as we approach the spring planting season in North America.

Nutrien was was established in January of 2018 by the merger of Agrium (primarily nitrogen fertilizers, but with a global retail network) and Potash Corp. (Saskatchewan, Canada has the largest recoverable potash deposit in the world). The two predecessor companies traded on average at more than 2x book value whereas at current prices Nutrien trades at just 1.4x book value. At 2.5x book value the stock should trade up to $95. In the meantime, the shares yield 3.5 per cent and the company will likely soon resume it’s share buyback program. Below is a quote from the third quarter earnings report:

“Nutrien delivered another quarter of solid operating results with strong fertilizer sales volumes and exceptional growth of orders through our digital agriculture platform, surpassing $1 billion of sales. Market conditions are improving around the world with higher crop and fertilizer prices, lower expected inventories and strong demand for crop inputs as we finish the year and enter 2021,” commented Chuck Magro, Nutrien’s President and CEO.

Nutrien Ltd. is expected* to report earnings for the fiscal Quarter ending Dec. 2020 on 02/17/2021 after market close. Based on what we know about industry fundamentals, this should be a very good earnings release. In fact, it is likely that (like the June and Sept. Quarters of 2020) there will be another positive earnings surprise above consensus estimates.

The best time to own this stock is before the strong summer growing season (peak earnings usually occur in the 2nd quarter).

Observers of the rocketing price moves of now familiar names, are describing the phenomena as ‘insane’ but it was bound to happen eventually. I’m just happy I’ve lived long enough to see some of these crooks get their comeuppance. Is ‘crooks’ a harsh word to use? Not in my opinion. For most of my career as an investment portfolio manager I loathed the idea that it was even possible to sell short – i.e. an investor borrows shares and immediately sells them, hoping to buy them back later at a lower price, return them to the lender and pocket the difference. For many companies out there defending their stock prices against short-sellers has been a futile exercise.

I often wondered why institutional fund managers didn’t long ago conspire to attack short-sellers in a similar fashion, but I suspect regulators would be all over them like dung beetles on poop if they did. It appears social media and determined individual investors (motivated by greed rather than divine justice but so-be-it) have managed to do the job and make lots of money in the process.

I love this quote from MarketWatch:

“Even if you don’t buy the argument that these short squeezes are temporary phenomena and that the prices will normalize, consider this: Shares of GameStop closed at $347.51 on Jan. 27. The company is expected to show a loss for calendar 2021, but a profit of $1.22 a share in calendar 2022. The business has its challenges because so many videogames are now downloaded, rather than purchased at stores. The pandemic has also, of course, hurt sales. But if we look back 10 years, the company’s best earnings came in calendar 2015, when it earned $3.86 a share. Even if GameStop were to improve its earnings to that level, the stock would be trading at a price-to-earnings ratio of 90.”

A company’s valuation by investors should be a reflection of its real financial and economic circumstances (okay, color me naïve), not solely determined by unscrupulous trading activity – in either direction. To date, the odds have favored the short-seller. But by aggressively forcing short–sellers to cover (a person with a short position must buy the shares, in this case to limit losses when the stock price unexpectedly goes up rather than down after being shorted) these gangs of young investors are giving short-sellers a taste of their own medicine.

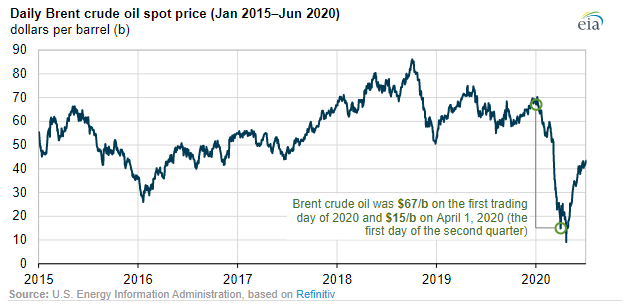

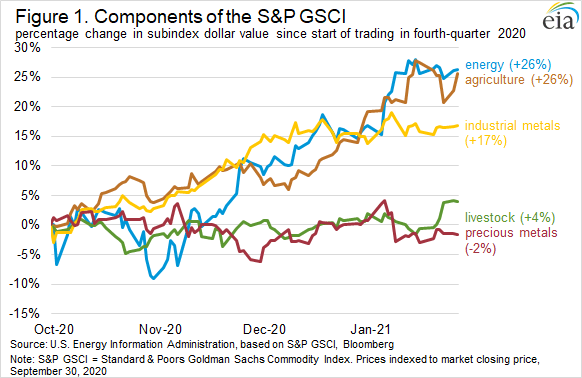

Meanwhile, there are good things happening in sectors that are being completely ignored. Despite the negative pressure on the energy patch caused by the current obsession with climate change, fundamentals continue to improve.

From the U.S. Energy Information Administration:

Energy prices have increased more than non-energy commodity prices on a percentage basis since October 2020.

Consider this from Joel Jackson, an analyst at BMO covering fertilizers and chemicals:

Name a fertilizer product – it’s likely rising this week (in some cases sizably). Fertilizer prices (mainly nitrogen and phosphate) have been surging on the back of continued strong crop prices, a long/strong fall season, and a strong expected northern hemisphere spring season.

Stocks like Suncor and Tourmaline (energy), Agrium (fertilizer) and Methanex have performed well for me, if lacking the rocket ship type charts of the names in the news, but its because their finances and economics are improving – yet the stocks are still cheap. And how about those lumber stocks I suggested some time ago.

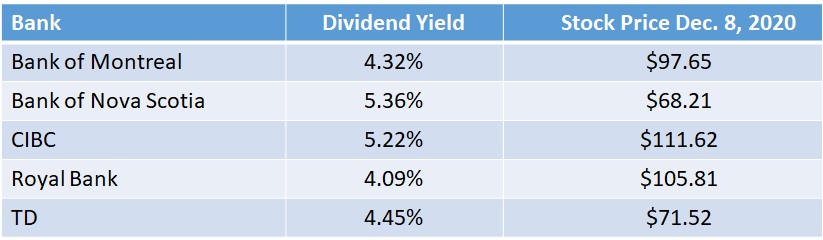

If you’re worried (as I am) that growth stocks (the tech and now healthcare stocks) are just ridiculously valued, then perhaps you should think about Canadian bank stocks as a potential cushion against a potential market correction.

Let’s face it, when mortgage rates are less than 2%, where can you park your savings and get a decent (above the rate of inflation) return?

Canadian bank stocks have staged an impressive rebound from the March (COVID-19) lows despite having set aside massive provisions for potential loan losses. They’ve all just reported earnings which were better than investment analysts were expecting. Most important, even at the higher prices they still offer dividend yields in excess of 4%.

Isn’t there a risk that they’ll experience losses as more businesses are unable to make commercial loan payments and unemployment disrupts mortgage revenues? In my experience the banks, which are ultra conservative when confronted with a crisis, tend to overshoot when estimating their loan loss provisions, meaning that as loan payments (that were estimated to go bad) from customers continue rather than go sour the provisions find their way back into earnings over time.

Banks make money on the spread between short term rates (or zero rates when it comes to your deposits) and what they can get in terms of interest income by lending the money out longer term. The fact that interest rates generally are so low (both short and long term) has hindered profitability to some extent. A steepening yield curve (meaning longer rates are rising) will also boost future profits.

Longer interest rates have begun to rise which bodes well for the banking sector in general.

There have been few opportunities over my long career where you can borrow money at a lower rate and invest it at a higher rate. Those lucky enough to have a homeowner’s line of credit (for example) charging 2% or less can use those funds to buy a basket of bank stocks and provided you document the money is indeed being used for investment purposes, the interest is tax deductible against your income. The income from dividends is taxed at a reduced rate. It’s a win-win.

Note from the stock prices how BMO (Bank of Montreal) was not long ago the worst performer of the group and is now one of the best. A word to the wise – over decades I’ve watched this trend over and over: The bank that trails its peers (that would be BNS now, evidenced by the highest dividend yield of the group) always manages to move ahead of the pack in subsequent years.

Back in early February, I posted an article suggesting Canadian lumber stocks were poised to perform. I mentioned that I’d bought one myself – West Fraser Timber (cost $57.85) – which is now just above $70. A 22% return over 6 months may seem trivial compared to some of the tech stocks, but I’ll take it.

My reasoning at the time was a reduction in duties imposed on exported lumber to the U.S, but the story now has more to do with a shortage of lumber. The lumber companies cut back (originally because of hefty duties) in anticipation of a possible plunge in the housing market due to the pandemic, but it turned out not to be as devastating as expected.

Soaring lumber and wood panel prices are adding thousands of dollars to the cost of building a home in Canada as strong renovation and new housing demand outstrip supply. (source CBC.ca)

If there’s a shortage of lumber in Canada, it is quite likely there’s also a shortage of wood product in the U.S., and since 30% of our product is exported south it bodes well for Canadian lumber producers.

There’s always a risk that Trump will increase duties, but with reduced costs (due to COVID-19) and layoffs it’s unlikely supply can ramp up and cause prices to decline; and very likely housing demand will continue to improve – bolstering profitability and ultimately share prices.

Names to consider include Canfor (CFP) West Faser Timber (WFT), Interfor (IFP), and Stella Jones (SJ). My own preference is WFT but I’ve also played the sector with IFP in the past.

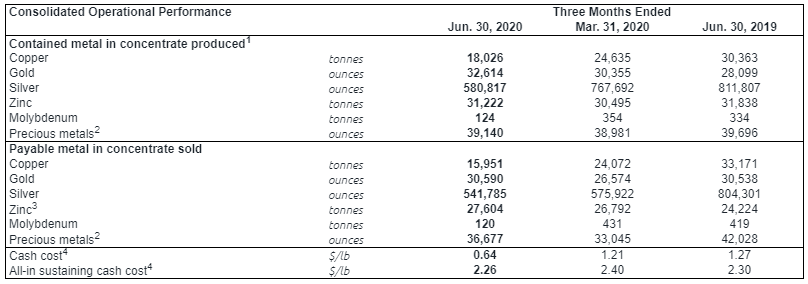

I borrowed the title from a Globe & Mail article. I first suggested buying into a metals recovery back in February suggesting Freeport (FCX) and Western Copper and Gold (WRN). One name I’ve also bought into is not on anyone’s radar screen. Hudbay Minerals (HBM) is a producer of a range of minerals in hot demand – copper, gold, silver zinc and moybdedum.

The company reported a loss in its most recent 2nd quarter which is not surprising. The loss would’ve been much less if they didn’t have to shut the Peru (Costancia mine) operation due to COVID-19. However, as I mentioned in my old book Resources Rock:

“Buy the stock when the company is losing lots of money, and sell the shares when they’re making more money than ever before.”

Retail sales continue to rebound despite the slow opening of the economy. Inevitably, many storefronts will not survive but those that do will be able to negotiate much more favorable terms when it comes to rent. The online capabilities of retailers with strong and growing brands have also been improved as they’ve had to adjust over the past several months.

Retail Sales – United States

The retail sales report showed 10 of 13 major categories increased, reflecting solid gains in furniture, electronics and appliances, clothing and sporting goods. Purchases at apparel shops jumped 105.1%, while electronics and appliances outlets saw a 37.4% gain. (Bloomberg.com)

Even in Canada, retail sales jumped 18.7% in May according to Statistics Canada. The two stocks – one a larger cap and the other a smaller cap – I believe should be owned are retail Canadian retail growth situations.

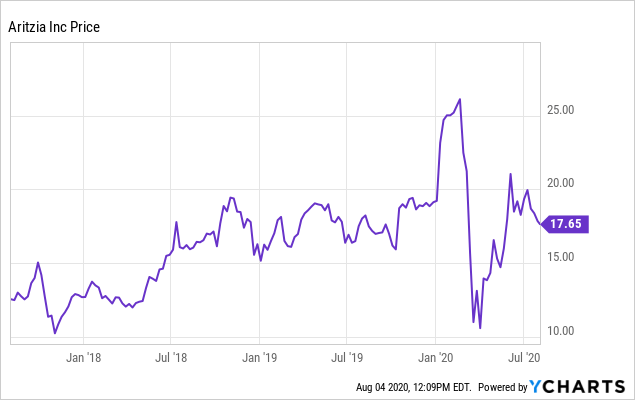

Aritzia Inc. (“ATZ” on TSX) – Smaller Cap Growth

COVID-19 restrictions caused the closing of all Aritzia stores (it’s been the bane of all retail) but since May 7th, 30 of its boutiques opened up again during its first quarter of 2021 and many more have opened since (89 of 96). Sales have been running about 55% to 65% of last year’s levels at the stores. Despite the difficult environment experienced, the company plans to open five to six new boutiques this year. Online sales surged 150% during the quarter – testimony to the power of their brand.

The key to continuing success is the strong financial position (Long-Term Debt to Equity is 24%) of the company. At the end of the quarter, it had $224 million in cash available with capital expenditure plans of only $35 million. With a bit over 109 million shares o/s and based on its recent share price, the market cap is $1.94 billion.

The stock has since recovered from the lows but remains about 35% below its pre-coronavirus levels. A precise valuation is difficult given the uncertainty going forward, however, the P/E based on 2020’s year end (a proxy for ‘normal’) EPS of 84 cents suggests a 21X multiple – which is reasonable for a business with its track record of consistent sales growth.

The company plans to continue penetrating the enormous US market and, recently, announced plans to open two new locations in New York and Los Angeles. An example of the attractive lease opportunities is the New York location:

The long-term lease in New York is on a prominent corner in Manhattan’s SoHo district, in a space that formerly housed luxury food shop Dean & DeLuca, and is costing Aritzia “25 to 30 cents on the dollar” compared with what it would have been two to three years ago. (Source, Globe & Mail, July 10th, 2020)

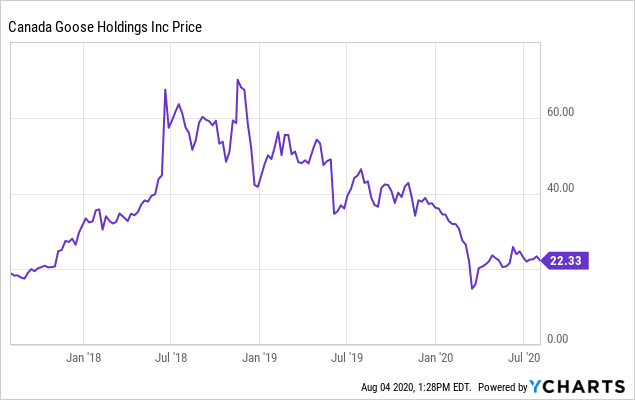

Canada Goose Holdings Inc. (GOOS) – Larger Cap

Canada Goose announced it will report its first quarter of 2020 results prior to the market open on Tuesday, August 11, 2020. We know the numbers won’t be pretty and may present a unique buying opportunity for this growing Canadian retailer.

Founded in a small warehouse in Toronto almost sixty years ago, Canada Goose has grown into one of the world’s leading makers of luxury apparel.

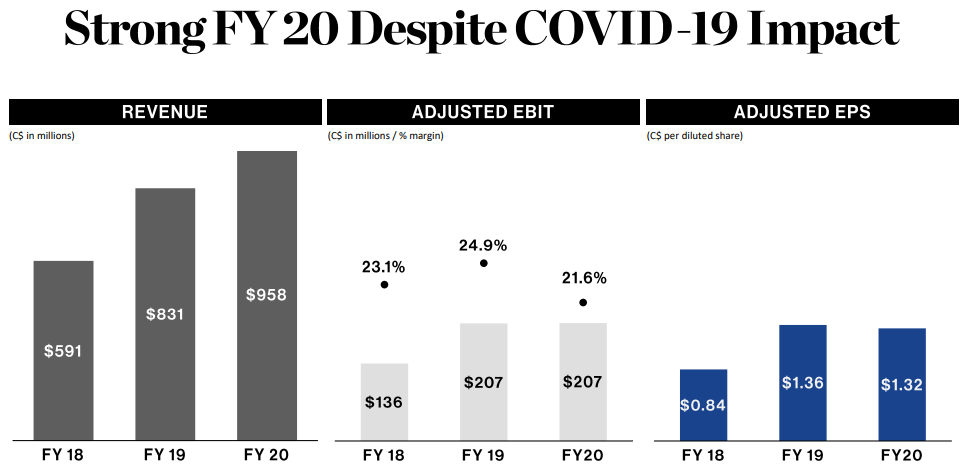

Adjusted EBIT was $207.4m, representing a 21.6% margin

Adjusted net income was $147.2m or $1.32 per diluted share

Acknowledging that their pending first quarter or the balance of this coming year will be anything but normal (will be ugly), the P/E using the 2020 EPS as a proxy of sorts suggests the stock is trading at roughly 17X. Market cap at current prices is about $3.3 billion.

The most exciting opportunity for GOOS is its foray into the Asian market. China, Japan plus South Korea account for just 21% of revenues but sales growth in that part of the world was 78% last year. China’s economy is widely known to have been rebounding nicely since it was hit by COVID-19 and should contribute to the company’s recovery over the next several quarters.

Target Prices – Through the Valley

I believe a conservative expectation for Aritzia is a resumption of its historical growth rate and per share earnings in the neighborhood of $1.15 2 years hence. At 25X earnings, my target over two years (I anticipate it will trade based on this EPS estimate this time next year) is $28. A 55% potential return.

My target for Canada Goose, arrived in a similar fashion, is $2.00 EPS and, with a 20X multiple, yields a $40 price for almost a 33% gain within 12 months.

Timing – Always Buy Retail in Summer Months

Seasonality should not be a surprise when it comes to investing in the retail sector. Canada Goose is famous for its winter luxury apparel (they’ve now expanded into footwear) which is hardly at the top of investors’ minds during the summer. In general, the shopping months (4th quarter) are when we will see revenue strength, and despite the pandemic, this year will be no exception.

The odds of better-than-expected retail profitability are quite good due to the operating leverage that surviving (and thriving) retailers have due to severe cost-cutting during the last several months (and ongoing). Salary reductions in the executive ranks, lower SG&A expenses, abatements on rent expenses, careful inventory management, and so forth will serve to improve margins materially.

Western Copper And Gold – Small Company With Huge Deposit

In a previous article (published in February) I suggested it’s wise to invest in copper highlighting two names. I discussed one large company, Freeport-McMoRan and a small Canadian exploration company developing a large copper/gold deposit in Canada’s Yukon called Western Copper and Gold (WRN). This time, I’d like to focus on the latter.

Since I posted that article, Freeport is up a modest 11%, but Western Copper and Gold has climbed 140%.

var tradingview_embed_options = {};

tradingview_embed_options.width = ‘640’;

tradingview_embed_options.height = ‘400’;

tradingview_embed_options.chart = ‘heeFetnE’;

new TradingView.chart(tradingview_embed_options);

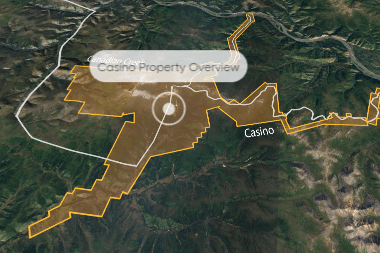

In its first estimate since 2010, Western Copper and Gold (TSX: WRN; NYSE-AM: WRN) has updated the resource for its 100%-owned Casino project in the Yukon with more drill results, confirming that it is one of the largest copper-gold deposits in the world. (Source: Mining.com)

WRN has about 122.4 million common (fully diluted) shares outstanding for a market cap approaching 200 million $CDN. It trades on the Toronto Stock Exchange and the NYSE American in $US. Its 52-week trading range on the Canadian Exchange is $0.44 – $1.90 ($0.31 – $1.53 on the American). Of course, like any exploration company, there are no revenues or earnings to speak of, but the company has $7.4 million in cash on hand.

The project is 100% owned, and its recently announced resource estimate is based on fresh drilling the company conducted in 2019, combined with results dating back to 2010 to 2012 that were previously not available. The resource now includes reserves of 7.4 billion pounds of copper and 12.7 million ounces of gold.

Already in the permitting stage, the mine has a minimum expected life of 22 years, a net present value of US$1.83 billion, and an IRR (after-tax) of 20.1%. With estimated cash costs net of by-products (for e.g. gold and molybdenum) of US$ -0.81/lb., the company should have no trouble raising the US$2.46 billion needed to fund the capex.

With several of the world’s larger mines on care and maintenance during the COVID-19 pandemic and China’s rapidly improving economy (the largest consumer of copper), it is inevitable that the gold/copper price ratio will rise from its currently depressed level – improving the net present value of these reserves and the economics of this massive deposit.

Trading at a fraction of its net present value (with a significant probability that continued drilling will grow the resource and that copper prices will strengthen), this microcap has plenty of room to rise from current levels.

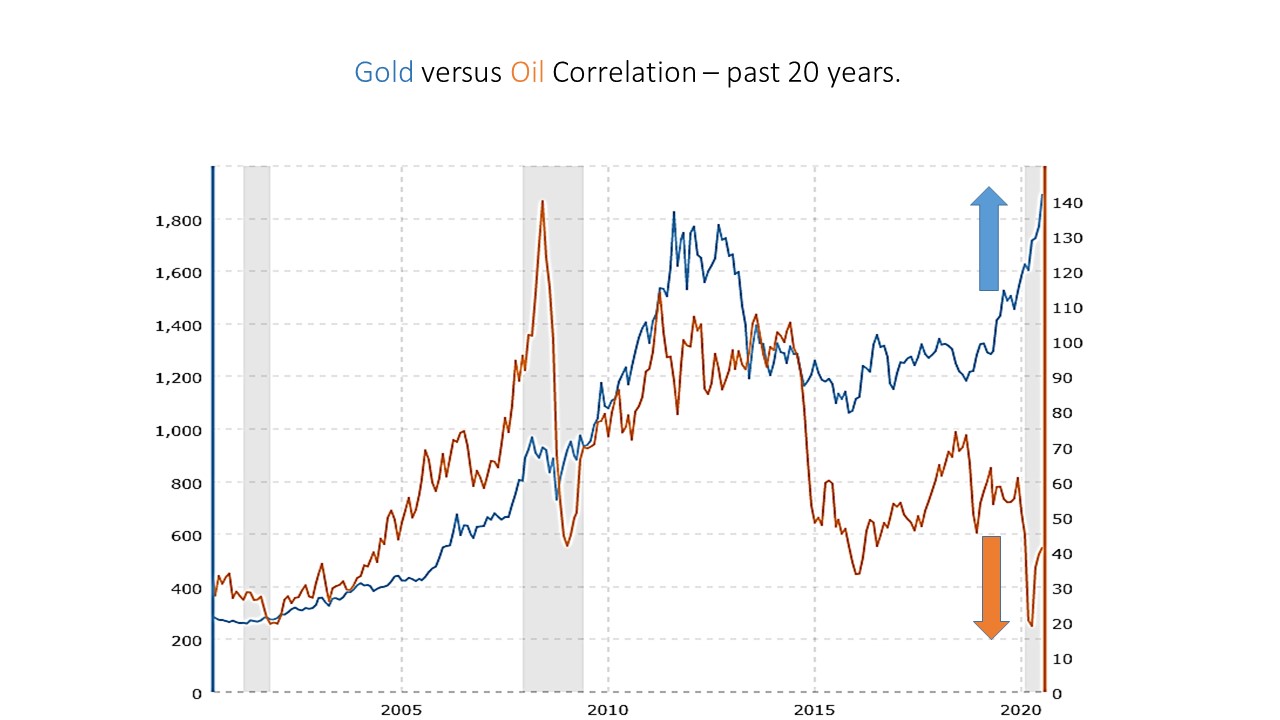

Until very recently, the oil price and gold price tended to follow a similar pattern, as evidence by the below chart. The fundamentals driving these prices differ of course, but over my many years I’ve come to expect the two to rise together, at times languish together and decline in tandem.

When I first bought a few gold stocks, the sector was washed out and companies were unable to raise any capital. Things have changed dramatically in recent months.

“Canada’s junior gold mining sector is on track for its best year for financing in nearly a decade as companies take advantage of soaring gold prices to load up on cash and advance long-delayed exploration and development projects.”

Globe & Mail July 27, 2020

Lack of investor interest is the best ‘buy’ signal I’ve used over the decades. It was lack of interest that inspired me to look at the gold sector when I did. The price of gold was creeping higher but nobody seemed to care.

We’re at that point now – where despite the stability of the price of oil, the stocks are of no interest to investors. Junior energy companies are struggling to raise capital – after all crude inventories are bulging (crude stocks are far above their 5-year average levels) and demand is constrained by COVID-19 right?

What will be the catalyst for the energy stocks to bounce back and resume their relationship with the price of gold? We’re already seeing production and development being curtailed by most companies, and OPEC+ has demonstrated the discipline necessary to re balance supply and demand in due course. Inventories of crude will be absorbed as economies continue to reopen and global trade is picking up steam. It is inevitable that the oil price will continue its climb from current levels.

What if the gold price declines? This is a distinct possibility – there’s so much hype now (in contrast to a year ago). However, the seemingly never ending onslaught of liquidity provided by central banks would suggest otherwise. As long as the opportunity cost of holding the precious metal is negligible, it is likely the price of gold will remain firm for the foreseeable future even if the big gains have already been had.

My own approach is to take profits in the yellow gold and invest the proceeds in black gold. There continue to be solid signs that economies are recovering which bodes well for Texas Tea.

Click on image to buy book at ChaptersIndigo online.

Available at bookstores, Amazon and for Kindle, at Kobo & iBooks.

Review

"This book is like Mal - who is a rider, a rocker and a rebel. He doesn't just think outside the box - he drags it behind his Harley on a cross-continent adventure and then runs over it a few times for good measure. The Bay and Wall Street guys are gonna hate it - Main Streeters should embrace it. One ton of fun!"

BJ Del Conte

Chase Producer, BNN - Business News Network

Business Producer/Anchor - CP24

Source:

Source:

Data by

Data by

Data by

Data by

We’re at that point now – where despite the stability of the price of oil, the stocks are of no interest to investors. Junior energy companies are struggling to raise capital – after all crude inventories are bulging (crude stocks are far above their 5-year average levels) and demand is constrained by COVID-19 right?

We’re at that point now – where despite the stability of the price of oil, the stocks are of no interest to investors. Junior energy companies are struggling to raise capital – after all crude inventories are bulging (crude stocks are far above their 5-year average levels) and demand is constrained by COVID-19 right?