If you’re worried (as I am) that growth stocks (the tech and now healthcare stocks) are just ridiculously valued, then perhaps you should think about Canadian bank stocks as a potential cushion against a potential market correction.

Let’s face it, when mortgage rates are less than 2%, where can you park your savings and get a decent (above the rate of inflation) return?

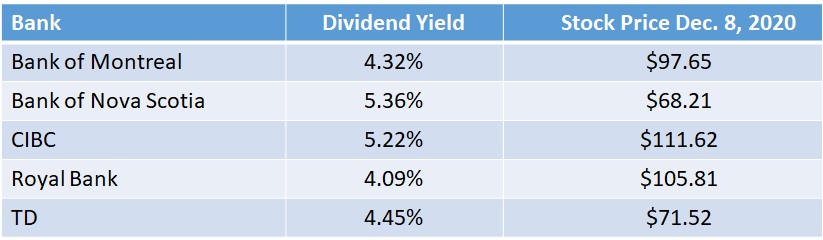

Canadian bank stocks have staged an impressive rebound from the March (COVID-19) lows despite having set aside massive provisions for potential loan losses. They’ve all just reported earnings which were better than investment analysts were expecting. Most important, even at the higher prices they still offer dividend yields in excess of 4%.

Isn’t there a risk that they’ll experience losses as more businesses are unable to make commercial loan payments and unemployment disrupts mortgage revenues? In my experience the banks, which are ultra conservative when confronted with a crisis, tend to overshoot when estimating their loan loss provisions, meaning that as loan payments (that were estimated to go bad) from customers continue rather than go sour the provisions find their way back into earnings over time.

Banks  make money on the spread between short term rates (or zero rates when it comes to your deposits) and what they can get in terms of interest income by lending the money out longer term. The fact that interest rates generally are so low (both short and long term) has hindered profitability to some extent. A steepening yield curve (meaning longer rates are rising) will also boost future profits.

make money on the spread between short term rates (or zero rates when it comes to your deposits) and what they can get in terms of interest income by lending the money out longer term. The fact that interest rates generally are so low (both short and long term) has hindered profitability to some extent. A steepening yield curve (meaning longer rates are rising) will also boost future profits.

Longer interest rates have begun to rise which bodes well for the banking sector in general.

There have been few opportunities over my long career where you can borrow money at a lower rate and invest it at a higher rate. Those lucky enough to have a homeowner’s line of credit (for example) charging 2% or less can use those funds to buy a basket of bank stocks and provided you document the money is indeed being used for investment purposes, the interest is tax deductible against your income. The income from dividends is taxed at a reduced rate. It’s a win-win.

Note from the stock prices how BMO (Bank of Montreal) was not long ago the worst performer of the group and is now one of the best. A word to the wise – over decades I’ve watched this trend over and over: The bank that trails its peers (that would be BNS now, evidenced by the highest dividend yield of the group) always manages to move ahead of the pack in subsequent years.

https://s3.tradingview.com/tv.js

var tradingview_embed_options = {};

tradingview_embed_options.width = ‘640’;

tradingview_embed_options.height = ‘400’;

tradingview_embed_options.chart = ‘tXiwVaI0’;

new TradingView.chart(tradingview_embed_options);